Organizations are moving rapidly from experimentation to embedded use of Generative AI (Gen AI), but value realization, governance, and workforce readiness are lagging the pace of adoption and investment as of Q4 2025, with a more disciplined and agent centric buildout likely in early 2026.

By the end of 2025, nearly every organization is using Gen AI, but most are still stuck in experimentation, fragmented tools, and shallow wins.

This first edition of the Sequencr Gen AI Adoption & Impact Index (GAII) cuts through the hype to show where real value is (and isn’t) showing up across adoption, ROI, governance, workforce behavior, and agentic workflows.

If you want a clear idea on what is changing in the world of Gen AI in 2026, then this is the index for you!

The first edition of Sequencr Gen AI Adoption & Impact Index (GAII) is here!

Organizations are moving rapidly from experimentation to embedded use of Generative AI (Gen AI), but value realization, governance, and workforce readiness are lagging the pace of adoption and investment as of Q4 2025, with a more disciplined and agent centric buildout likely in early 2026.

We will be providing quarterly updates on the latest Gen AI statistics and trends, so make sure to register your interesthere to be notified of updates.

Adoption accelerated, but it’s uneven and fragile

By late 2025, Gen AI is broadly adopted but unevenly integrated:McKinsey reports nearly 90% of organizations using AI, with use of Gen AI in at least one business function, jumping to 71% in 2024. Yet most firms have not scaled it into core operating models. S&P's Global research notes rapid rollout plans but also high project failure rates as organizations seek to go from proof-of-concept to implementation and impact.

Process change lags behind tool usage, complex tasks see bigger wins

However, there were some positive use cases where Gen AI has seen greater value and impact – work such as design and prototyping, sales outreach, and internal system interaction versus popular areas such as content creation. These more complex tasks and processes are often associated with agentic frameworks, suggesting that we may see more applications in 2026.

The market continues to feed the fire

Investment and market momentum remains intense, with global AI spending projected by Gartner to reach $2.53 trillion in 2026 and $3.33 trillion in 2027, driven largely by infrastructure and compute investment as organizations continue scaling AI from experimentation into core operating environments.

Workforce behavior is outpacing governance

Workforce behavior is running ahead of policy, as Microsoft’s Work Trend Index, indicates roughly 75% of knowledge workers use AI, often via self-provisioned tools. Meanwhile, leadership urgency is rising but structured training and change management continue to lag.

McKinsey reports only 21% report redesigning workflows around Gen AI, and only 27% requires human review of all Gen AI content. These lower adoption levels are complimented with 47% reporting negative consequences from Gen AI use.

As for governance and risk frameworks, they are consolidating but remain patchy in execution: OECD and other regulators are pushing interoperable risk-based approaches and richer incident tracking, while S&P Global highlights elevated failure and stagnating KPI performance tied to weak monitoring, security, and bias controls.

Lookahead: Q1 2026 Gen AI Landscape: Shifting from Experimentation to Industrialization

“Consolidate and control” becomes the default for enterprises

Over the period of experimentation, organizations invested in various tools. With better clarity and as organizations seek to improve outcomes, expect more organizations to reduce tool sprawl, formalize approved stacks, and tighten review of tools.

Marketing and comms shift from “content generation” to “content systems"

Organizations with AI adoption will look into:

Knowledge bases and retrieval workflows

Brand voice guardrails coupled with QA (human oversight)

Measurement frameworks (quality, cycle time, risk)

Governance pressure rises despite not having a global standard

Policy activity is accelerating and incident tracking is rising. In 2026, leaders will be pushed to show control and manage risks. There’ll be more focus on embedding AI governance within operations from workforce skilling, processes, and data (“AI Ops”) as differentiators rather than hygiene factors.

Agentic workflows creep into real work

Expect more “multi-step” workflows to move from pilots to light production within organizations as we move to more successful agentic solutions.

If you want to dig into these trends or learn more about Gen AI solutions, book a meeting with us to jumpstart your journey today.

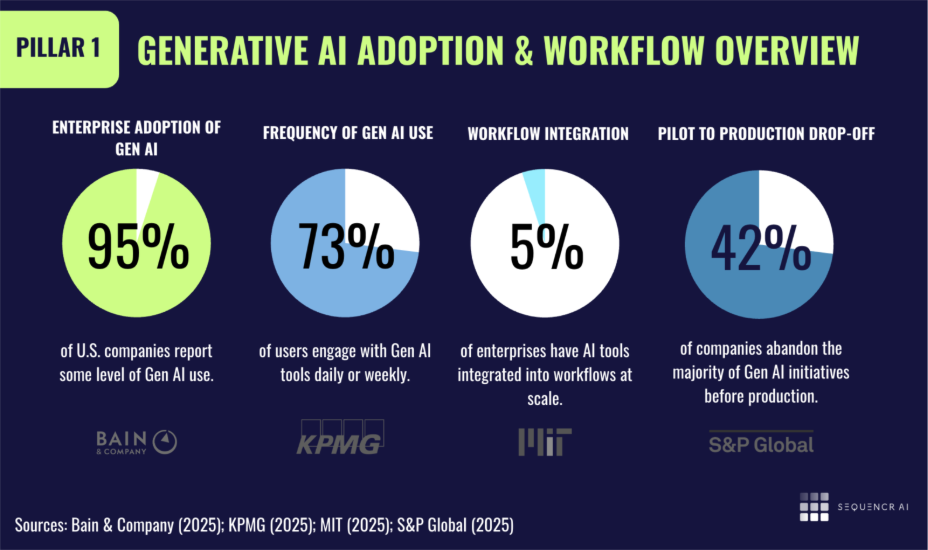

Pillar #1: Adoption & Workflow Integration

The first pillar tracks adoption progress from scattered Gen AI tools and pilots to deep embedding in end-to-end workflows. It reveals the gap between "having AI" and "AI being strategically implemented into everyday tasks", where leading firms scale value through strategy, data, talent, and process changes. For marketing and comms teams, it's the discriminator between simple content generation and AI-orchestrated systems

McKinsey’s 2025 State of AI survey shows AI has moved into the operating mainstream, with about 78% of organizations using AI in 2024 (up from 55% in 2023) and 71% using Gen AI in at least one business function. However, only 5% of enterprises have embedded it deeply in end-to-end workflows.

S&P Global reports that as organizations race to deploy Gen AI, the share abandoning most initiatives before production jumped from 17% to 42%, signalling a gap between pilots and durable operating change.

Wharton AI Adoption 2025 confirms 82% of enterprise leaders use Gen AI weekly, 46% daily, 87% enterprises (10K+ employees) implemented AI, yet most remain in the experimentation phase.

On the positive side, The Federal Reserve Bank of St. Louis confirms workplace Gen AI adoption hit 37.4% in Q3 2025 (up 4.1pp YoY), outpacing PCs/internet at equivalent lifecycle stages, reinforcing that while adoption is accelerating, durable workflow integration remains the binding constraint.

BCG AI at Work 2025 reveals 72% of employees are regular AI users (several times weekly/daily), but frontline adoption stalls at 51%, showing enablement, not access, as the bottleneck.

Stanford’s AI Index notes global AI optimism in countries like China (83%), Indonesia (80%), and Thailand (77%) see AI products and services as more beneficial than harmful. In contrast, optimism remains far lower in places like Canada (40%), the United States (39%), and the Netherlands (36%). Since 2022, optimism has grown in previously skeptical countries, like Germany (+10%), France (+10%), Canada (+8%), Great Britain (+8%), and the United States (+4%).

Signals of Operating Model Change

As many struggle to maintain long-lasting Gen AI adoption, there is hope for those looking to start:

McKinsey’s “Rewired” research highlights that scaled value correlates with changes across strategy, operating model, technology, data, talent, and adoption practices rather than standalone tools, implying that genuine operating change is concentrated in a minority of “AI - Mature” firms.

Deloitte’s 2025 predictions indicate roughly 25% of enterprises using Gen AI are expected to deploy AI agents in 2025, with agentic systems moving beyond pilots in some markets—an early sign of workflow level automation rather than individual task assistance.

Bain’s research reported Gen AI growing adoption in the United States with 95% companies using it, where production use cases have doubled, with IT seeing the fastest growth. As IT-led implementations scale, Gen AI is more likely to drive durable operating change by reshaping how work is orchestrated across functions.

Q1 2026 Outlook

Expect a pivot from scattered pilots to platform-led integration: Gartner anticipates CIOs shifting from bespoke Gen AI builds to commercial solutions embedded in existing enterprise platforms. These changes should increase integration depth even as “AI specific” software line items become harder to isolate.

As agentic AI matures, frontline workflows will increasingly be redesigned around AI-assisted processes (for example, sales, service, research), but adoption will likely remain bimodal: a cluster of “frontier” firms integrating AI into core processes, while laggards stay in tool-use mode.

As Gen AI systems increasingly shape discovery and summarization, marketing and comms teams continue to structure content for retrievability by AI systems, extending internal retrieval and RAG principles to external-facing content. With only 21% of organizations having redesigned workflows around Gen AI, this reinforces a growing gap between firms experimenting with AI and those redesigning content as part of an operating system. Learn more about mapping out GEO in 2026 here.

Generative AI Adoption and Workflow Overview

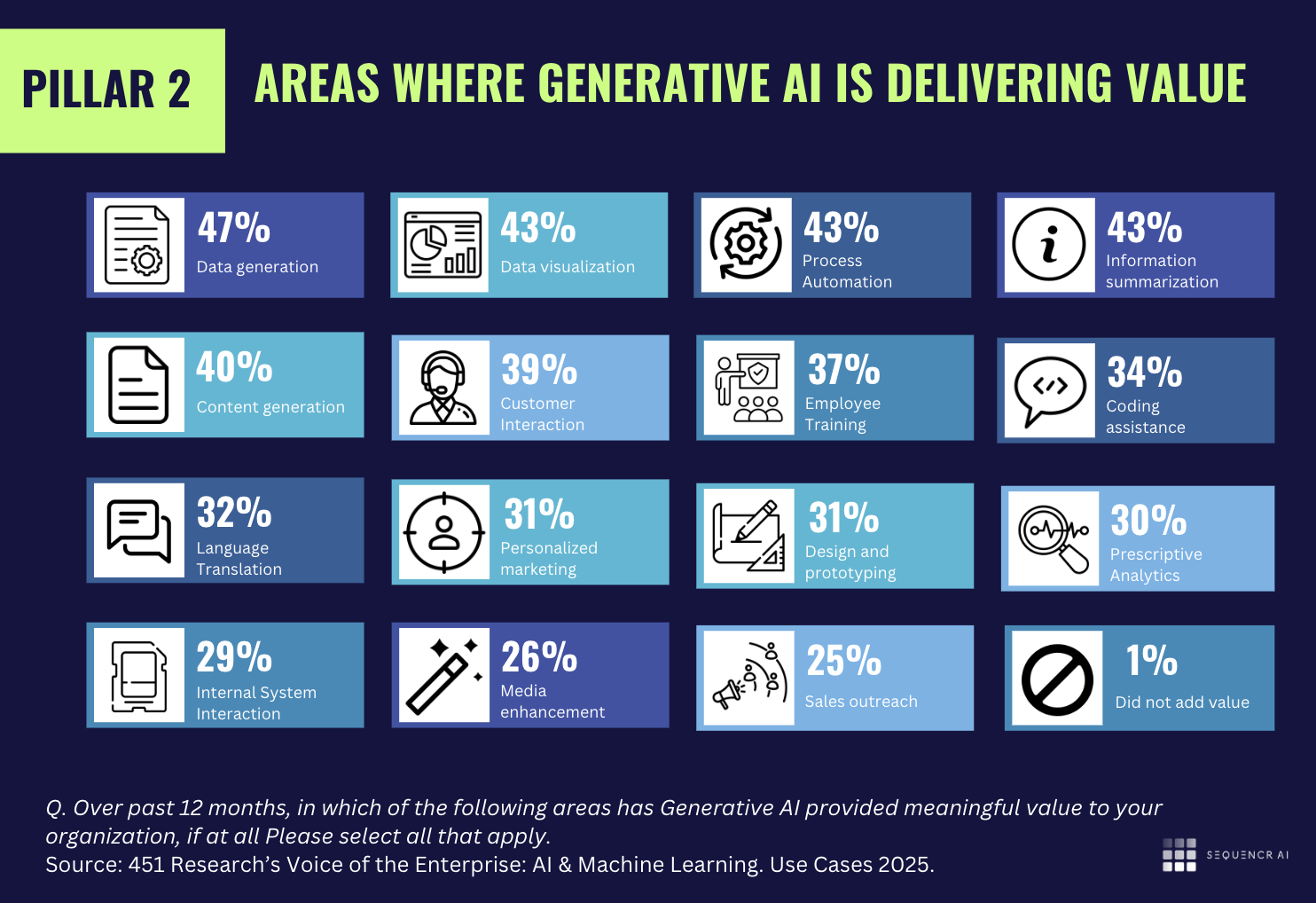

Pillar #2: Value Realization

The second pillar assesses progress from Gen AI experimentation to measurable cost, revenue, and productivity outcomes at workflow and enterprise levels. It exposes the gap between individual time savings and firm-wide ROI, where leaders succeed by pairing AI with clear use case prioritization and operating model rewiring.

Current Value Signal

MIT Sloan’s 2025 AI & Data Leadership Executive Benchmark suggests 58% of data and AI leaders believe their organizations have achieved “exponential” productivity or efficiency gains from AI, indicating perceived value but also some optimism bias.

At the same time, S&P Global finds that among organizations investing in Gen AI, 46% report no single enterprise objective with a “strong positive impact,” highlighting that realized, measurable value remains elusive for many.

Knowledge at Wharton finds 72% now formally measure ROI (productivity/profit focus) and 75% leaders see positive returns, but 43% worry about skill degradation without operating rewiring, reinforcing that improved measurement alone has not resolved the gap between localized gains and enterprise-level impact.

BCG's analysis reveals 60% of firms see minimal ROI from AI investments, while 5% 'future-built' leaders capture 5x revenue gains and 3x cost reductions through innovation beyond automation.

Cost, Revenue, and Productivity

McKinsey’s work links scaled AI value to management practices such as clear use case prioritization, change management, and talent strategies, implying that productivity and revenue benefits emerge only when AI is paired with operating model rewiring rather than point solutions.

External country level data, such as KPMG’s 2025 Generative AI Adoption Index in Canada, shows 79% of workplace users self-report meaningful productivity gains and over half report saving 1–5 hours per week. While only 2% of business leaders say they see a clear return on AI investment—underscoring the gap between individual time savings and enterprise level ROI.

On a positive note, BCG’s AI Radar notes four out of five CEOs are more optimistic about the ROI of their AI investments than they were a year ago, while nearly all CEOs believe that AI agents will produce measurable returns in 2026. As CEO confidence in agent-driven ROI rises, leadership may become more willing to accept workflow disruption and role redesign in pursuit of larger gains, reducing resistance to deeper operating-model change.

Q1 2026 Outlook

A minority of organizations that standardize on a smaller set of high ROI use cases (for example, customer support automation, coding assistance, document workflows) will begin to see measurable cost and revenue gains, while others stall in fragmented experimentation.

There is growing pressure from boards, regulators, and investors, for hard metrics on AI investments, which should push teams to move from experimentation metrics (usage, satisfaction) to business outcomes (unit cost, cycle time, NPS, revenue per employee) in early 2026.

As AI investment scales, organizations will face growing pressure from boards, finance leaders, and investors to demonstrate hard value metrics tied to cost, revenue, and risk. McKinsey notes that organizations capturing the most AI value are significantly more likely to link AI initiatives to clear business KPIs and to embed change management and workflow redesign alongside deployment, while others struggle to move beyond localized productivity gains. This is expected to accelerate in early 2026 as AI budgets come under greater scrutiny.

Areas Where Generative AI is Delivering Value

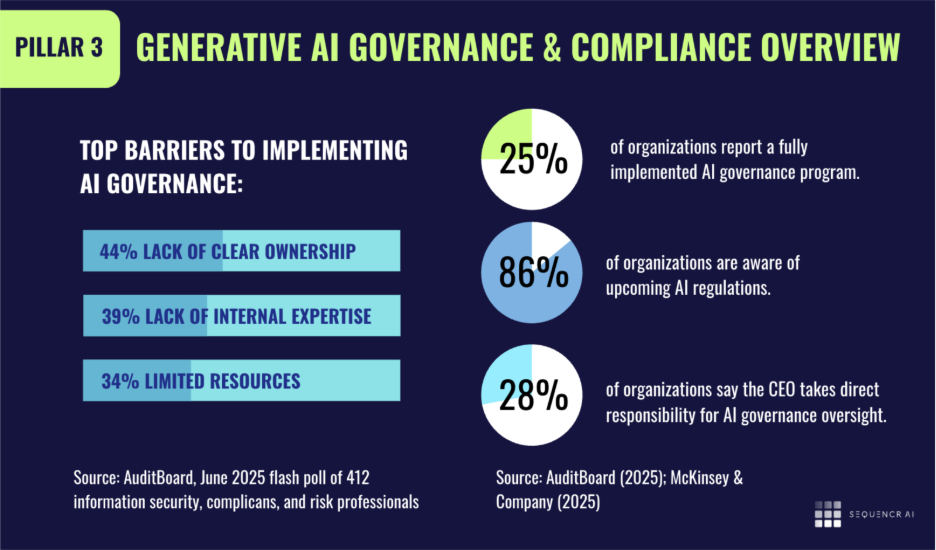

Pillar #3: Governance, Risk & Trust

The third pillar tracks the shift from static AI policies to operational controls managing bias, security, performance, and incidents through monitoring and human oversight. It reveals the gap between paper compliance and production-ready trust, where mature firms use registries, audits, and risk frameworks aligned to OECD/NIST standards. For marketing and comms teams, it's the discriminator between ad-hoc content review and scalable systems that protect brand reputation under regulatory scrutiny.

Risk and Governance Landscape in Q4 2025

The OECD’s AI principles stress accountability and have been operationalized through tools like the AI risk management interoperability framework and an expanding catalogue of tools and metrics for trustworthy AI, which promote a structured approach to defining, assessing, mitigating, and monitoring AI risks.

S&P Global notes that organizations with more mature monitoring, tailoring, and security practices outperform peers, while high failure rates and stagnating KPI performance are often linked to weak controls over data privacy, bias, security, and model performance.

BCG observes that Gen AI is being adopted in a highly decentralized manner across business units, often outpacing formal risk and compliance structures. Instead of slowing adoption, leading organizations are beginning to embed Gen AI directly into risk and compliance workflows themselves, using it for monitoring, documentation, testing, and control design.

AuditBoard research highlights a growing execution risk in AI governance driven by inverted sequencing. While 45% of organizations invest in AI usage monitoring, 44% in risk assessments, and 40% in third-party model evaluations, only 28% maintain usage logging, 25% document models, and 23% enforce access controls — reiterating advanced oversight is often built without the operational foundations needed for durable governance.

Regulatory and Policy Momentum

Stanford’s AI Index documents rising concern about AI misuse and calls out intensified regulatory activity and scrutiny, particularly in data protection, safety, and content integrity, which drives demand for more formal governance structures inside enterprises. In 2024, U.S. federal agencies introduced 59 AI-related regulations and issued by twice as many agencies. Globally, legislative mentions of AI rose 21.3% across 75 countries since 2023.

Major government and multilateral bodies (for example, OECD and national digital government guidelines) increasingly emphasize responsible Gen AI use in public services, which indirectly shapes enterprise expectations for transparency, documentation, and incident response.

Despite high awareness, AI governance execution lags: 92% of organizations report confidence in third-party AI visibility, yet only around 66% conduct formal risk assessments and just 25% have fully implemented governance programs, with unclear ownership (44%), limited expertise (39%), and limited resources (34%) emerging as the primary constraints.

Q1 2026 Outlook

Expect governance to shift from static policies to operational “AI control planes,” as organizations standardize model registries, approval workflows, monitoring dashboards, and incident reporting pipelines for AI applications.

Trust is likely to become a differentiator: customers and partners will increasingly demand evidence of robust risk management and assurance (for example, audits, bias and safety testing), favouring firms that have professionalized AI governance rather than treating it as ad hoc compliance.

OECD analysis suggests that as AI becomes embedded across decision-making, service delivery, and oversight, governance will increasingly shift toward anticipatory risk management and institutional resilience. In early 2026, this is likely to elevate AI governance into a strategic capability focused on foresight and long-term trust preservation.

Gartner projects AI governance will consolidate around trust-based, execution-level control systems. By 2027, they predict 60% of data governance teams are expected to prioritize unstructured data for Gen AI, and by 2028, 80% of S&P 1200 organizations will relaunch governance programs around trust models. Today, 74% already use data governance tools to operationalize AI governance.

Generative AI Governance and Compliance Overview

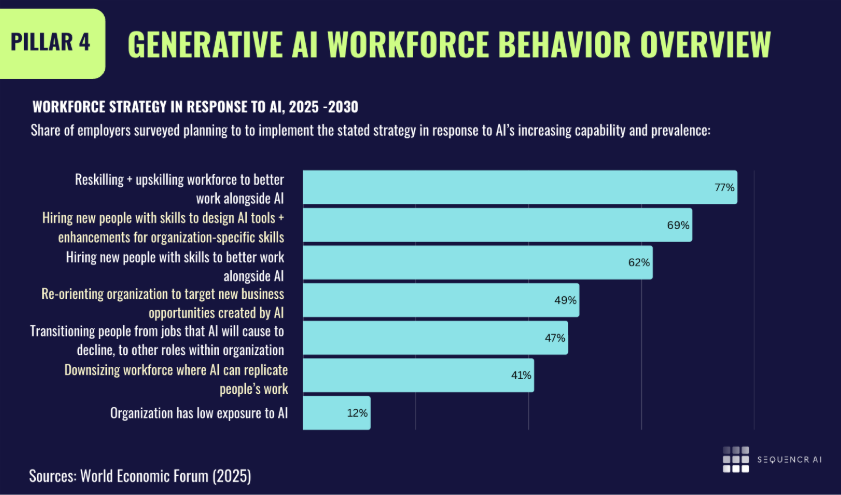

Pillar 4: Workforce & Behavior

The fourth pillar examines employee Gen AI usage, such as frequency, tool preferences, and shadow AI prevalence, against formal policies, training adequacy, and emerging role changes. It captures the gap where 45% of employees now use AI at work (up from 40% in Q2 2025), requiring cognitive and digital upskilling over narrow AI expertise.

Actual Usage vs. Policy

Microsoft’s 2025 Work Trend Index finds that about 75% of knowledge workers are already using AI, and a large share prefer their own tools over employer provided options, indicating substantial “shadow AI” (or the unauthorized use of AI tools, models, or platforms by employees without their company's IT or security team's knowledge or approval) usage beyond formal policies.

The same research shows that 90% of AI “power users” say AI saves them time, and 85% start or end their workday with AI, revealing deep behavioural integration even where organizational processes and training are still catching up.

BCG’s 2025 AI Adoption research suggests that Gen AI is still surface‑level for most workers: more than 85% remain in basic task assistance and delegation modes, and fewer than one in ten have reached semiautonomous collaboration where agents reshape workflows instead of just answering prompts.

BCG also reported that 54% of employees say they use AI tools even when not formally authorized, reflecting significant shadow AI use that outpaces policy and training. Additionally, only 36% feel adequately trained and just 25% of frontline staff report clear guidance from leadership. These stats highlight a workforce that is experimenting faster than governance and enablement can keep up.

Skills, Training, and Sentiment

OECD work on AI and skills suggests that most workers exposed to AI need stronger management, cognitive, and digital skills rather than specialized AI skills, with demand for these capabilities rising in AI-exposed occupations; however, there are emerging signs that demand patterns are shifting as AI tools diffuse.

Country-level studies, such as KPMG’s 2025 index, show that 83% of employees feel the need to upskill to use Gen AI tools effectively, while less than half believe their organization provides adequate support, highlighting a sizeable training and enablement gap. In Canada, 51% of Canadian employees use Gen AI (index score 36.74, +22pts since 2023), 79% report productivity gains, but 83% need upskilling while only 48% get organizational support.

KPMG business leaders survey (753 Canadian execs) reveals only 35% strongly agree employees have skills to leverage Gen AI fully, while just 37% say organizations mandate AI training, confirming the enablement shortfall.

McKinsey Global Survey 2025 reveals 88% of organizations now use AI in at least one function (up from 78% last year), but only 38% have scaled beyond pilots—highlighting the skills gap between experimentation and enterprise impact.

BCG reports only 36% of respondents are satisfied with AI training, while only 25% of frontline employees feel leadership support on usage, yet 5+ hours training boosts regular usage by 12–19pp, confirming skills as primary ROI drag.

Q1 2026 Outlook

Expect more structured AI skills programs and new roles: Microsoft’s analysis forecasts 50% of managers expect AI upskilling to become a core team responsibility within five years, with 78% of leaders planning AI-specific hires like trainers, prompt engineers, and agent specialists by mid-2026.

Workforce behavior will likely remain ahead of formal policy, so organizations that align incentives, training, and safeguards with how employees use AI, rather than attempting to suppress usage, will gain a productivity and talent attraction edge.

World Economic Forum Future of Jobs 2025 forecasts 77% of employers will reskill workers for AI between 2025-2030, with 69M new AI-adjacent roles created despite 83M displaced—net positive but requiring rapid upskilling.

PwC AI Jobs Barometer 2025 shows AI skills command 28% wage premiums across industries, with wages rising twice as fast in AI-exposed sectors, which is driving structured training demand into Q1 2026.

Generative AI Workforce Behaviour Overview

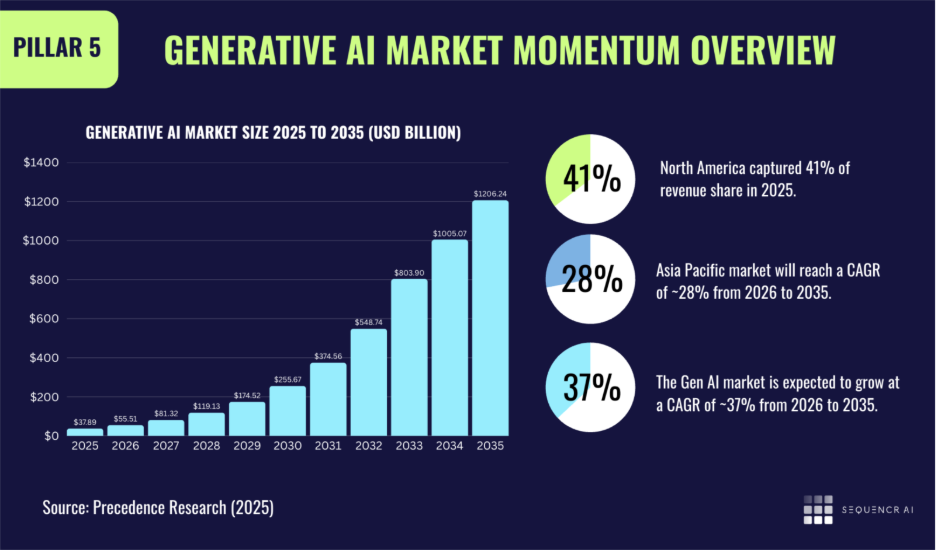

Pillar 5: Market & Capability Momentum

The fifth pillar monitors external forces, such as investment flows, capital expenditure, and agentic model advances, that expand Gen AI's technical feasibility for enterprise workflows. It tracks the shift from horizontal tools to vertical/domain-specific solutions plus hardware buildout enabling "default" capabilities, like real-time personalization.

Investment and Innovation Intensity

Stanford’s AI Index reports that total corporate AI investment reached about USD 252.3 billion in 2024, with private AI investment up 44.5% year on year and newly funded Gen AI startups nearly tripling, indicating a still accelerating innovation and funding environment.

Gartner expects global Gen AI spending to rise about USD $2.5 Trillion in 2026, with a 44% increase year-over-year, with nearly 80% directed to hardware (devices and servers), underscoring the buildout of AI capable infrastructure as a foundational capability shift.

BCG’s research reveals agentic AI already drives 17% of total AI value (rising to 29% by 2028), with frontier firms allocating 15% of budgets vs. nearly 0% for 60% of laggards, revealing a market momentum around advanced capabilities

Menlo Ventures Q4 2025 reports $18B enterprise app spend doubled Year-over-year, signaling capital flowing to vertical/agentic solutions over generic tools.

BCG's analysis reveals leaders reinvest aggressively (26% more IT spend, 64% higher AI budgets) into capabilities like agentic AI (17% of value now, doubling to 29% by 2028), creating virtuous momentum. The rest face vicious cycles of constrained investment and competitive erosion.

Labour Market and Macro Shifts

The World Economic Forum’s 2025 Future of Jobs analysis projects that AI and related technologies will transform 86% of businesses by 2030, creating about 170 million new jobs while displacing 92 million, and rendering roughly 39% of current skill sets outdated between 2025 and 2030.

OECD evidence indicates that AI changes the task mix in many jobs and boosts demand for management, business, and digital skills, yet also finds early signs that demand for some of these skills may plateau or decline as AI tools become more capable.

Q1 2026 Outlook

Market momentum will increasingly favour agents and verticalized solutions: Deloitte expects 25% of enterprises using Gen AI to deploy AI agents in 2025, rising to 50% by 2027, while Gartner forecasts strong growth in specialized, domain specific models for particular industries.

Stanford’s AI Index notes that nearly 90% of notable AI models in 2024 came from industry, up from 60% in 2023. Model scale continues to grow rapidly, training compute doubles every five months, datasets every eight, and power use annually. This means the frontier is becoming increasingly more competitive and increasingly crowded for the next big model to come to light.

As capital markets and boards get more discerning about AI ROI, capability momentum will shift from generic experimentation to deeper integration of AI into sector specific workflows (for example, healthcare, financial services, manufacturing), with accompanying investments in data quality, infrastructure, and domain-tuned models.

BCG 2026 forecast expects agentic AI to drive 29% of enterprise value as boards demand ROI proof, accelerating shift from generic tools to vertical workflows with 26% higher IT and capital expenditure commitments from frontier firms.

Generative AI Market Momentum Overview

Use Cases: Where We’ve Seen Gen AI Applied

Enterprises are concentrating Gen AI in a handful of repeatable, high leverage workflows from customer support, software development, sales/marketing, R&D, finance, to internal knowledge work, and are starting to measure impact with clear productivity, quality, and financial KPIs. These are some examples where companies have applied and measured impact:

Sales, Marketing & Customer Growth

Where Gen AI is Applied

Drafting outbound emails, proposals, and account plans; summarizing call transcripts and surfacing risks/opportunities in CRM.

Personalizing website, ad, and lifecycle messaging content at scale; generating audience specific variations.

Impact Evidence & Metrics

Microsoft’s Work Trend Index highlights customer service, marketing, and product development as top investment areas through 2026, with “frontier firms” using AI heavily for marketing and customer success workflows.

Typical metrics:

Productivity: campaign build time; number of tailored assets produced per marketer; proposal turnaround time.

Growth: email open and reply rates; pipeline created; win/close rates; uplift in conversion vs. Non-AI campaigns.

Financial: CAC, marketing ROI, revenue per seller.

How Companies Operationalize Measurement

Holdout tests: AI generated vs. Human only sequences or creatives, comparing conversion and revenue.

Time to produce and pipeline conversion dashboards tied to AI usage (for example, % of opportunities with AI generated summaries).

Company Examples

LinkedIn: Applies AI across sales and customer growth workflows, including account insights, lead prioritization, and outreach recommendations. LinkedIn reportshigher seller productivity and improved relevance of outreach, based on internal performance tracking and product usage signals, without publishing a single universal uplift metric.

HubSpot: Uses Gen AI to automate lead scoring, email drafting, and campaign personalization. HubSpot reportsimproved conversion rates and higher marketer productivity based on customer surveys and usage data, with adoption measured across thousands of marketing teams rather than a single controlled experiment.

How Leading Firms Frame Measurement

Across these use cases, it’s important to note these starting points:

Start with a specific workflow, not “AI in general” (for example, first level support chat, invoice collections, outbound sales, incident response).

Define 2–3 primary KPIs per workflow (one productivity, one quality, one financial) and capture baselines for 8–12 weeks.

Roll out GenAI in controlled pilots (teams, regions, product lines) and run A/B or before/after comparisons with sufficient volume.

Tie AI usage telemetry (for example, which agents use the tool, prompts per day, suggestions accepted) back to KPIs to isolate

These patterns align well with your index pillars: the same use case level metrics can roll up into value realization (Pillar 2), workforce behaviour (Pillar 4), and even governance (Pillar 3) when you layer in quality, error, and risk indicators.

About Sequencr Gen AI Adoption & Impact Index (GAII)

The Gen AI Adoption & Impact Index (GAII) is Sequencr’s quarterly synthesis and interpretation of the most relevant signals on how enterprises are moving from Gen AI experimentation to real operating change. GAII draws on published benchmarks and enterprise signals, organized into a consistent framework so leaders can track momentum quarter to quarter.

Rather than viewing AI adoption as a single metric, GAII expands the lens to include five pillars that represent the key conditions for transformative Gen AI and sustained impact:

Adoption and workflow integration

Value realization

Governance, risk, and trust

Workforce enablement and behavior

Market and capability momentum

The index is designed to highlight where Gen AI is delivering impact, what’s working, and where leaders should focus, beyond tool adoption, on the constraints that matter most. This index is updated quarterly to reflect new benchmark data, shifts in enterprise practices, evolving governance approaches, and changing skill expectations tied to the future of work.

Get the full report here – X pages full of reputable statistics exploring Generative AI adoption and trends, right at your fingertips!

Subscribe to our newsletter for exclusive Generative AI insights, strategies, tools, and case studies that will transform your marketing and communications.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Subscribing confirms your agreement to our privacy policy.